Immediate tax, uncertain returns: Unravelling the Unacademy ESOP shock

The firm’s management said exercising these options will convert them into common shares and keep open the chance of receiving equity in the merged company.

Experts and employees point out that exercising forces an immediate tax bill on illiquid shares and may still leave former employees with nothing once investor protections are honoured.

The result is a stark, high-stakes choice for people who believed their ESOPs might one day deliver upside.

What changed

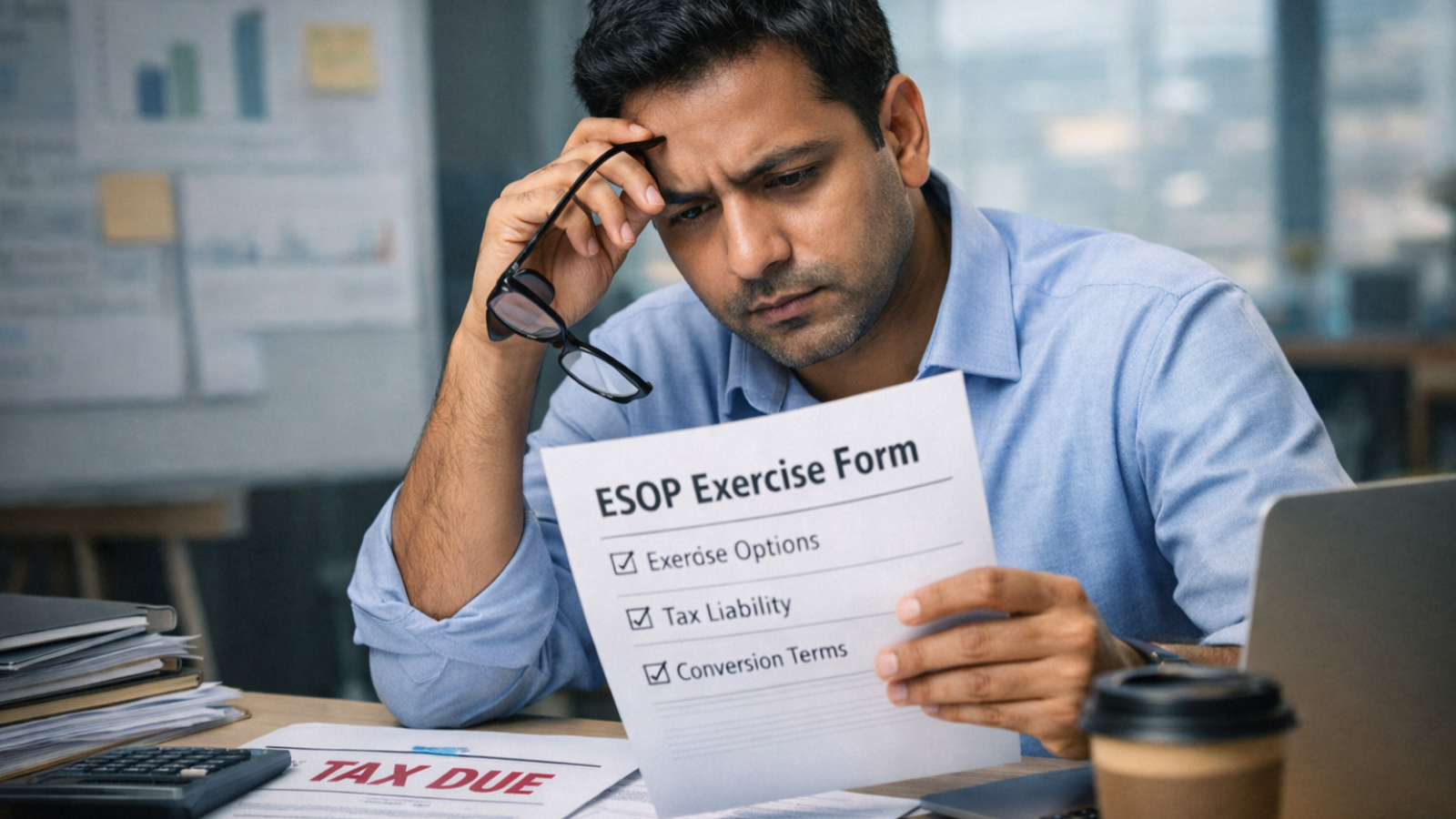

Unacademy asked exited employees to exercise their vested options so that those options become common equity before any stock-based deal is completed.

Co-founder and CEO Gaurav Munjal explained the reasoning in an internal note. He said the proposed transaction is an all-stock deal, meaning the buyer would pay using its own shares rather than cash, and that the valuation being discussed is far lower than earlier fundraising rounds.

upGrad has placed a bid to acquire Unacademy at a valuation of $300 to 400 million, as reported by YourStory earlier. For context, Unacademy was last valued at $3.4 billion after raising $400 million from Japan’s SoftBank Group in 2021. It has raised over $800 million in funding across multiple rounds.

Because of this, investors are expected to invoke liquidation preference. Liquidation preference is a contractual right that allows investors to be paid before ordinary shareholders in a sale.

The stated aim of asking employees to exercise is to ensure that exited employees are treated the same as other common shareholders, such as founders and current employees, if the merger goes ahead.

What exercising means for tax and liquidity

Exercising an option means using the right to buy shares at a pre-set price known as the exercise price. This step turns an option, which is only a promise of possible shares in the future, into actual shares today.

Under Indian tax rules, this moment is treated as income. Tax is calculated on the difference between the share’s fair market value, which is the value assigned to the share for tax purposes, and the exercise price, which is usually much lower.

As a result, many former employees must pay tax immediately, even though they cannot sell these shares right away and may never receive cash from them if investor protections take priority in a sale.

Why an all-stock deal changes the economics

In a cash deal, sellers are paid money when the transaction is completed. In an all-stock deal, there is no cash payment. Instead, sellers receive shares in the company that is buying them.

This means that only people who are shareholders at the time the deal closes will receive shares in the buyer in exchange for their existing shares. An unexercised option is not a share and therefore usually does not take part in such a swap unless it has been exercised and converted into a share beforehand.

This is why Unacademy management has pushed for exercise. Converting options into common shares allows holders to be treated the same as long-term common shareholders in any share swap. What it does not guarantee is how much value common shareholders will actually receive once investor rights are applied.

How liquidation preference works

Investors who bought preferred shares usually have contractual rights that put them first in line in any sale, merger or liquidation. A common version is a one-time liquidation preference, which means investors are entitled to get back at least the amount they invested before common shareholders receive anything.

In practice, this works like a waterfall. Investors are paid first and recover the money they are owed. Only if some value remains does it flow to common shareholders. If the sale value is not enough to cover what investors are owed, common shareholders may receive nothing at all. Exercising options only moves an employee into the common shareholder group. It does not reduce or change what investors must be paid first.

The tax math

Here is a simple example.

Assume a share is valued at Rs 500 for tax purposes and the exercise price is Rs 10. The employee is taxed on Rs 490. If the applicable tax rate, including cess, is 33%, the employee must pay about Rs 160 in tax immediately.

If, after the deal is completed and investors are paid first, those shares end up being worth only Rs 0 to Rs 50, the employee would have paid Rs 160 in tax for shares that may be worth far less.

This is why many former employees believe exercising feels like spending real money today for a highly uncertain payoff.

Why management says this is necessary

Unacademy’s management presents the exercise window as a practical attempt to prevent ESOPs from becoming completely worthless. The chief executive said that if liquidation preference is fully enforced, unexercised options would effectively go to zero.

By converting vested options into common shares, the company highlighted that it is giving exited employees parity with other common shareholders in any stock-based merger and preserving at least a theoretical claim on any remaining value.

Management has also noted that founders and investors would not receive cash in an all-stock deal and that this outcome was not desired. The company is offering a way to remain part of the ownership structure rather than a cash payout or a guaranteed return.

What critics are saying

Former employees and independent observers highlight some concerns. Exercising creates taxable income today on shares that may never generate cash. Becoming a common shareholder does not change the fact that investor preferences are likely to absorb most or all of the deal value. Exercising does not bring meaningful cash into the company, so it does not improve the balance between investor claims and common equity.

Ravi Handa, an entrepreneur and a former employee at Unacademy, explained in X posts how exercising converts options into common shares that exist on paper, but those shares may still be worth nothing once liquidation preference is applied. The question many are asking is why they should pay tax now for a conversion that could leave them worse off.

What former employees should ask

Employees affected by the change should seek clarity on how exercised shares will be treated in the deal and how they would convert into the buyer’s shares, ideally in writing before exercising, according to experts.

They should also ask whether a cashless exercise is possible, whether tax support will be offered to cover liabilities, and whether the exercise window can be extended with a clear timeline.

Before taking any irreversible step, it is sensible to consult a tax adviser and a lawyer who specialises in employee equity. Professional advice can help model tax outcomes and show how different liquidation preference scenarios might play out.

What this means for the ecosystem

This episode underlines that ESOPs are not simply deferred bonuses. They are legal and financial instruments whose value depends on ownership structure, investor rights and the nature of the exit.

Asking exited employees to exercise during merger talks is unusual and exposes the tension between investor protections and employee expectations.

Edited by Jyoti Narayan

Discover more from News Link360

Subscribe to get the latest posts sent to your email.